With regard to health insurance coverage, people who have persistent health concerns or need routine medical attention should try to find policies with lower deductibles. Though the yearly premium is higher than an equivalent policy with a higher deductible, more economical access to medical care throughout the year may be worth the compromise.

Know the standard types of insurance coverage for people. Name and describe the various sort of organization insurance coverage. Certain terms are usefully defined at the outset. InsuranceAn agreement of reimbursement. is an agreement of repayment. For instance, it repays for losses from specified hazards, such as fire, typhoon, and earthquake. An insurance providerThe entity that accepts provide insurance for the risk of particular type of losses, generally life, property, health, and liability claims. is the business or person who assures to repay. The guaranteedThe person or company guaranteed by a contract of insurance. What is commercial insurance. (in some cases called the ensured) is the one who receives the payment, other than when it comes to life insurance, where payment goes to the beneficiary named in the life are timeshares a good investment insurance contract.

The agreement itself is called the policyThe contract for the insurance sought by the guaranteed. The events guaranteed against are referred to as threatsPossible losses that might be covered by policies of insurance. or hazardsThreats that are insured versus. Regulation of insurance coverage is left mainly in the hands of state, instead of federal, authorities. Under the Mc, Carran-Ferguson Act, Congress excused state-regulated insurance provider from the federal antitrust laws. Every state now has an insurance department that supervises insurance coverage rates, policy requirements, reserves, and other aspects of the industry. For many years, these departments have come under fire in lots of states for being ineffective and "captives" of the industry.

From time to time, efforts have actually been made to bring insurance coverage under federal guideline, but none have been effective (What is liability insurance). We start with an introduction of the kinds of insurance coverage, from both a customer and a business point of view. Then we examine in higher information the three most essential kinds of insurance: residential or commercial property, liability, and life. Sometimes a distinction is made between public and private insurance. Public (or social) insurance consists of Social Security, Medicare, short-term special needs insurance, and so forth, moneyed through government plans. Private insurance strategies, by contrast, are all kinds of protection provided by private corporations or companies. The focus of this chapter is private insurance.

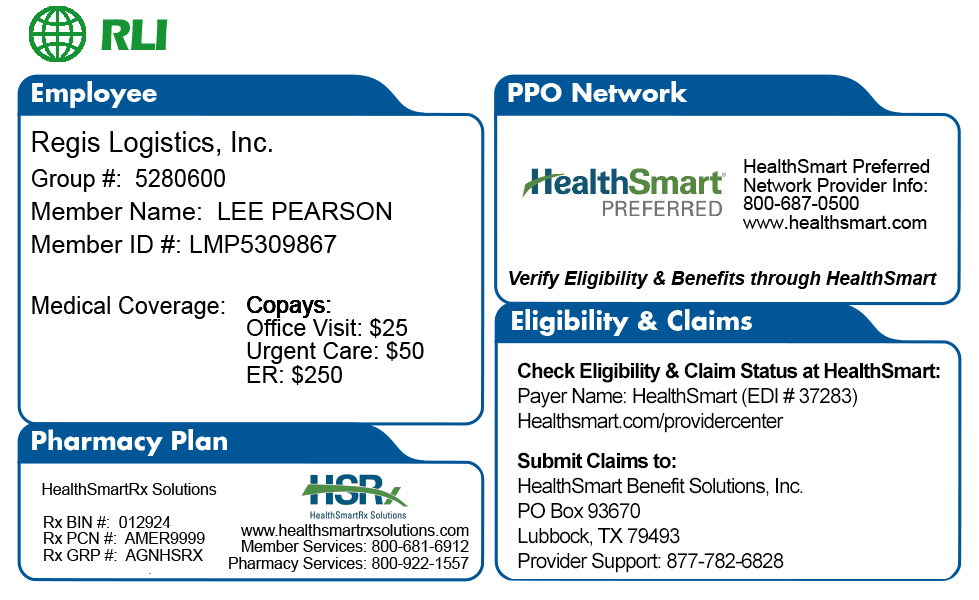

Two basic types are available: term insuranceLife insurance with a death advantage but no built up savings. provides protection only throughout the term of the policy and settles only on the insured's death; whole-life insuranceSupplies cost savings in addition to insurance coverage and can let the insured gather before death. offers cost savings in addition to insurance and can let the insured gather prior to death. Health insurance covers the cost of hospitalization, sees to the medical professional's workplace, and prescription medications. The most useful policies, provided by many companies, are those that cover one hundred percent of the costs of being hospitalized and 80 percent of the charges for medicine and a doctor's services.

6 Simple Techniques For How Much Is House Insurance

Twenty years ago, the deductible might have been the first $100 or $250 of charges; today, it is frequently much higher. A disability policy pays a specific portion of a staff member's wages (or a repaired amount) weekly or month-to-month if the employee becomes not able to work through illness or a mishap. Premiums are lower for policies with longer waiting periods prior to payments should be made: a policy that begins to pay a handicapped employee within thirty days might cost twice as much as one that postpones payment for 6 months. Website link A homeowner's policy provides insurance coverage for damages or losses due to fire, theft, and other named perils.

The property owner should assess his requirements by aiming to the likely risks in his areaearthquake, hailstorm, flooding, and so on. House owner's policies offer reduced protection if the property is not guaranteed for at least 80 percent of its replacement expenses. In inflationary times, this requirement suggests that the owner must change the policy restricts upward each year or acquire a rider that instantly adjusts for inflation. How much is pet insurance. Where property worths have actually dropped considerably, the owner of a house (or a commercial building) might discover cost savings in decreasing the policy's insured amount. Vehicle insurance is perhaps the most commonly held type of insurance.

The normal car policy covers liability for bodily injury and property damage, medical payments, damage to or loss of the automobile itself, and lawyers' charges in case of a lawsuit. In this litigious society, an individual can be demanded almost anything: a slip on the walk, an extreme and incorrect word spoken in anger, an accident on the ball field. An individual liability policy http://griffinlikq597.image-perth.org/the-main-principles-of-why-is-my-car-insurance-so-high covers lots of types of these risks and can give coverage in excess of that supplied by homeowner's and car insurance. Such umbrella coverage is usually relatively inexpensive, maybe $250 a year for $1 million in liability.

Some might do this through self-insurancethat is, by setting aside certain reserves for this contingency. Most smaller sized companies purchase employees' compensation policies, available through industrial insurance companies, trade associations, or state funds. Any business that uses automobile need to keep a minimum of a minimum auto insurance coverage on the automobiles, covering injury, property damage, and basic liability. No organization must take a possibility of leaving unprotected its structures, long-term components, machinery, inventory, and so forth. Numerous property policies cover damage or loss to a business's own home or to residential or commercial property of others stored on the properties. Experts such as doctors, attorneys, and accounting professionals will typically purchase malpractice insurance coverage to safeguard versus claims made by dissatisfied clients or customers.

Depending upon the size of business and its vulnerability to losses arising from damage to important operating equipment or other residential or commercial property, a company may wish to buy insurance coverage that will cover loss of incomes if the service operations are interrupted in some wayby a strike, loss of power, loss of raw product supply, and so on. Businesses deal with a host of dangers that might result in significant liabilities. Many types of policies are readily available, including policies for owners, property owners, and occupants (covering liability incurred on the facilities); for manufacturers and contractors (for liability sustained on all properties); for a business's products and finished operations (for liability that arises from warranties on products or injuries triggered by items); for owners and professionals (protective liability for damages triggered by independent specialists engaged by the insured); and for contractual liability (for failure to follow efficiencies needed by specific agreements).

Unknown Facts About What Is Epo Insurance

Today, the majority of insurance coverage is readily available on a plan basis, through single policies that cover the most important risks. These are frequently called multiperil policies. Although insurance is a requirement for each United States business, and lots of businesses operate in all fifty states, guideline of insurance has actually stayed at the state level. There are several kinds of public insurance coverage (Social Security, impairment, Medicare) and many forms of personal insurance. Both people and organizations have substantial needs for various types of insurance coverage, to supply security for health care, for their property, and for legal claims made versus them by others. Theresa Conley is joining the accounting firm of Hunter and Patton in Des Moines, Iowa.